Frequently Asked Questions

A. General Questions

[collapsibles]

[collapse title=”1. What is Oiconomy Pricing and what is covered?”]

Oiconomy pricing is a full cost accounting methodology that measures the hidden costs of a product. These costs express the burden that the product places on planet and people, that are currently not represented in the economic price of a product. Oiconomy pricing measures the costs to prevent any negative impact from happening and reveals the costs to make the product fully sustainable. The cost to prevent any negative impacts is expressed in the unit “ESCU” (Eco Cost Social Unit), which can be transferred into any currency.

The method integrates the Sustainable Development goals (SDG’s) set by the United Nations.

Example:

A cup of coffee costs € 2 euro. The production of a cup of coffee is associated with deforestation, climate change and unfair payment. Making the cup of coffee free of any of those sustainability impacts induces extra costs. This would add 50 cents to the price, making the full costs for the cup of coffee € 2,50

[/collapse]

[collapse title=”2. What are the benefits?”]

- Each aspect of your production through the value chain is identified in terms of prevention: What should be done to avoid negative impacts and the costs of doing that now can be discussed in negotiations with your suppliers.

- No vague sustainability score (yes/no labels), no narrative story about sustainability activities and plans, but growing towards a concrete quantitative score, representing the cost-distance to sustainability. If no verifiable evidence can be demonstrated, unsustainability is assumed.

- Hidden costs are identified for all sustainability aspects, in line with the 17 UN Sustainable Development Goals. Due to this comprehensive nature, you will be prepared for all aspects.

- In a widely used Oiconomy system, by comparing your full cost with the average in your markets, you can show your level of frontrunner-ship.

- Harmonised assessment and reporting throughout the supply chain which will lead to communication and cooperation within the supply chain through one common language.

- Trustworthy and transparent supply chains, as results of upstream suppliers are transferred to the next supplier leading to a full cost picture at the end-producer.

- Various expenditures, benefitting the society, adhering to certain criteria, can be allocated as positive cost.

- Through the Oiconomy Assessment tool companies can execute the assessment independently, or with little support.

- A mainstream Oiconomy system enables selection of supply chains by their score.

[/collapse]

[collapse title=”3. What is the difference to other assessments and certifications?”]

Difference to ISO certifications

ISO certifications are standards that can verify compliance to set criteria. ISO standards (e.g. ISO 14000) exists that focus solely on the environmental domain. These standards aim for an effective environmental management system but do not state requirements for environmental performance or measure the environmental performance. Oiconomy Pricing is a sustainability assessment that quantifies the performance per product on all levels of sustainability. It only requires trustworthy measurement and verifiable data. Based on Oiconomy Pricing, you can improve and monitor your sustainability improvements.

On some aspects Oiconomy Pricing does accept other certificates as evidence for sustainable behaviour.

Difference to Life Cycle Assessment (LCA)

Most LCA’s quantify the environmental performance of a product. LCA calculates the impact of a product (such as in CO2 equivalents, Phosphorus and Sulphur dioxide). It does this by measuring the consequences on the environment due to production. Oiconomy Pricing does not measure the consequences of production on the environment but focusses on costs of preventing any impact from happen in the first place. We believe expressing sustainability in prevention costs is more suitable for sustainability assessments as they steer the conversation on what should be spent in the supply chain to avoid any negative impact. Additionally, most LCA’s only quantify the environmental dimension of sustainability and Oiconomy pricing covers the planet, people and prosperity pillar.

Difference to other True Price methodologies

Oiconomy pricing differs from other true pricing methodologies in scope, data, transparency, and assurance.

- Oiconomy Pricing includes more social sustainability aspects than any other true pricing methodology. It measures aspects such as human health, occupational health & safety, financial responsibility, corruption & conflict and fair taxes, whereas other methods only include a few of those aspects.

- The data that is used in Oiconomy pricing is as much as possible supply-chain specific data and aims for companies to provide their own mitigation costs, whereas other methodologies are more reliant on general databases.

- Oiconomy Pricing developed the Oiconomy Assessment tool, which is a tool companies can use to calculate their own hidden costs. This means that the company can execute the assessment more independently than other methods.

- Oiconomy Pricing is a non-profit foundation tied to Utrecht University that is fully transparent about the methods and the underlying data and assumptions, whereas other methods often do not disclose this.

- The goal of Oiconomy pricing is to increase effective supply-chain collaboration by giving the supply-chain partners a tool that standardises and quantifies sustainability performance. This creates a common language for the supply-chain. Other full cost accounting methodologies do not give such tools for supply-chain collaboration.

- The Oiconomy pricing is a tool similar to financial bookkeeping and intended to be applied yearly.

[/collapse]

[collapse title=”4. How do I get started?”]

If you are considering applying Oiconomy Pricing please contact us. We will schedule a meeting to get to know each other and check for suitability to apply Oiconomy Pricing. The next round of pilots with Oiconomy Pricing is scheduled to start in September 2022.

[/collapse]

[collapse title=”5. What do I need to start?”]

Oiconomy Pricing is developed to be suitable to any product or service, in any industry for any company. However, in order to successfully conduct the Oiconomy Assessment there are several conditions:

- Transparency: For accurate calculations the organisation will need to be fully transparent on their activities. This includes e.g. amount paid to suppliers and wages of employees. These data remain confidential and only need to be available for the project leader for Oiconomy Pricing inside the company, as well as for the Utrecht University-team.

- Data availability: The assessment needs as much supply-chain specific data as possible, and it is beneficial for the assessment to already have data available before the start of the assessment. This is especially applicable concerning (small) suppliers that do not have capacity to execute the Oiconomy Assessment themselves, for instance smallholder farmers. If data is not available there is the possibility for it to be collected or to use data from databases

- Capacity in the organisation: Executing the Oiconomy assessment takes time. While the time intensity differs based on data availability and complexity of the product, it is estimated that the first assessment takes 80 hours to complete over the span of 3-4 months. Next assessment will be much easier and faster.

[/collapse]

[collapse title=”6. What support is offered?”]

The Oiconomy Team is available for support during the Oiconomy Assessment. We are creating a team of student ambassadors, comprising of master’s students in Sustainable Business and Sustainable Development from the Utrecht University that will be available to assists companies through the process.

[/collapse]

[collapse title=”7. Who inside my company needs to be involved ?”]

The Oiconomy Assessment needs to be championed by an employee within the organisation. This usually concerns an employee working in the sustainability or procurement department. Furthermore, the assessment needs data on material use, electricity consumption, water use, as well as data on employees, finances and suppliers. Collecting these data points usually requires involvement of the HR department, financial department, quality assurance manager, product category manager, procurement & suppliers’ relations.

[/collapse]

[collapse title=”8. What data do I need?”]

The exact data need per company depends on the location, the product and the place in the supply-chain. Generally, the following data points needs to be collected.

General data

Data needs to be available on general production metrics such as: production volumes, product revenues and costs per product unit.

Planet

Data needs to be collected on any resource used by the company, and generated waste and other outputs. This includes the use of electricity, land, water, and materials. Already calculated emissions regarding the product can also be entered into the system directly.

People

Data needs to be collected on public health, product quality management, labour circumstances (wages, over hours, pension plans, health insurance, personnel development, occupational health & safety and various other labour conditions).

Prosperity

Data needs to be collected on the amount paid to suppliers, compliance to financial criteria, paid taxes and the governance of corruption & conflict.

[/collapse]

[collapse title=”9. How are my suppliers involved?”]

The main suppliers will need to be involved in Oiconomy Pricing and calculate the hidden cost for their product. Suppliers will go through the exact same process as your organisation.

Not all suppliers of the product need to calculate their hidden costs. Oiconomy Pricing has come up with a method to determine what suppliers need to be involved. To find out what suppliers need to participate the 80% rule is applied. The end-producer needs to make a list of all purchased materials and services related to the product. This list needs to be sorted from highest purchased value to lowest. The suppliers who are present in the list containing 80% of the purchased value of the product need to be involved in making the assessment to uncover their hidden costs.

Example:

- Simple: For 1 kg of green coffee 80% of the purchased value of coffee is from buying the coffee beans from farmers. This means that only the supply-chain of coffee beans needs to be included.

- More complex: 80% of the purchased value from 1 jar of white pepper comes from the pepper, the jar and the cap. This means that the supply-chain of pepper, the jar and the cap needs to be included.

See examples for more details

[/collapse]

[collapse title=”10. Who can see my completed Assessment?”]

The data entered the system is fully confidential and not visible to the public or any other actors into the supply chain. The results of the assessment: the hidden cost per sustainability category are shared with the next actor in the supply chain. In this way a full hidden cost picture emerges at the end of the supply-chain. Individual company data behind the calculates is kept private.

A disclosure agreement is signed between the company and Utrecht University that specifies the amount of disclosure the company is comfortable with. In the light of open science, which is to make science transparent and accessible to everyone, the minimum disclosure is a fully anonymised case summary with hidden cost specified per sustainability aspect that is publicly available.

[/collapse]

[collapse title=”11. What sort of claims can I make based on the results?”]

Companies may only communicate their hidden costs if the data are verified by an external body (certification). Companies may not make any claim that contradicts the result of the assessment.

[/collapse]

[collapse title=”12. How much time does it take?”]

The time it takes to execute the Oiconomy Asssessment differs based on data availability and complexity of the product, bookkeeping, management support and experience with standards and assessments. Generally, for first time users the Oiconomy Pricing Assessment takes a maximum of 80 hours per company to complete, over the span of 3-4 months. This includes time spend by the Oiconomy project lead as well as the necessary support from other departments. Furthermore, each assessment requires an estimated 60 hours of support from the Utrecht University team. Next assessments may be a routine operation and bookkeeping with the company that is completed fast.

[/collapse]

[collapse title=”13. What methodology is used?”]

The Oiconomy methodological justification sheets describe each indicator and specify the assumptions, used data and formulas. These justification sheets will be posted soon.

[/collapse]

[collapse title=”14. How do ‘positive costs’ work?”]

Besides negative hidden costs, a product can have positive effects on planet and people. Positive costs are based on actual company spending, benefitting others than the ones involved in the transaction. A positive externality occurs when a third-party benefits from activities or consumption of a product without contributing to the (full) costs of the transaction.

Strict criteria for allocation of positive costs are formulated in the publication on assessment of positive impacts by Pim Croes and Walter Vermeulen. Companies can receive positive costs on among others the following indicators:

- Beneficial products sold below cost price (e.g. medicines for the underprivileged).

- Quantity of captured CO2 (e.g. in organic agriculture).

- Recycling of disposed products from other organisations.

- Development of environmental sustainability enhancing products or technology.

- Restauration and/or long term protection of natural ecosystems or upgrading of soils/land.

- Contributions to the local social development around the organisation.

- Provision of medical or mental care.

- Protection of cultural heritage and indigenous people or stimulating cultural activities.

- Costs from providing micro credits below cost price.

- Cancellation of debts to the underprivileged.

- Capacity raising education to others than those working for the organisation.

- Employing people with distance to the labor market.

- The surplus of paid wages above the Fair Minimum Wage in the 20% poorest countries in the world.

- Infrastructural investments or services without negative environmental or social impact and without economic benefits for the organisation itself.

[/collapse]

[collapse title=”15. How accurate are the results?”]

Within the Oiconomy Pricing Assessment there are two types of data that can be differentiated. The first one is performance data. Performance data express the environmental, social and economic performance of a company. This data is entered by companies in the Oiconomy Assessment tool that indicate their activities (e.g. amount paid to employees and kWh used). Companies need to provide as much company-specific performance data as possible. If a company cannot supply specific data, then generic data-based sourced data is used. The generic data-based sourced data is often based on location and industry of a company but makes the results less accurate than company-specific data.

The second type of data is prevention costs. Having identified the sustainability impacts, prevention costs express the costs of a preventative measure (e.g. installing solar panels, restoring biodiversity or paying fair wages). Companies can input their own mitigation costs, but if that is unavailable generic data-based sourced costs for preventative measures are used.

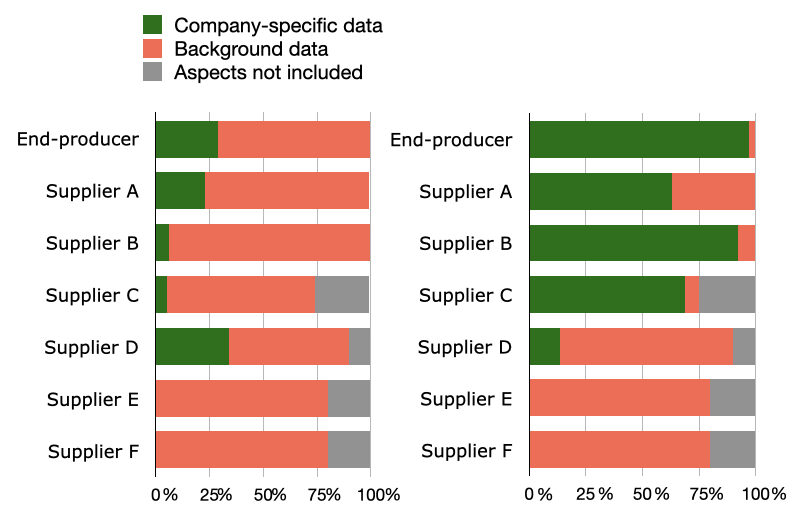

In each assessment the accuracy of performance data and prevention costs is reported to indicate the accuracy of the assessment (Figure 1 & 2).

Figure 1: Performance data. Figure 2: Prevention costs

[/collapse]

[collapse title=”16. Is Oiconomy Pricing a standard/ certification scheme?”]

Oiconomy Pricing is in developed to become an accredited standard, that can certify companies through audits. This part of the future developments of Oiconomy Pricing.

We are always looking for partners to collaborate with us, please contact us if interested.

[/collapse]

[collapse title=”17. What are future developments?”]

Oiconomy Pricing is in the development stage and is being piloted. Plans for future developments can be found here.

[/collapse]

[collapse title=”18. What is the connection with (future) policies and legislation?”]

In 2011, a first global authoritative standard on the business responsibility to respond human rights was endorsed by the UN Human rights council. The UN Guiding Principles on Business and Human rights (UNGPs), state that it is not enough for businesses to comply to state laws but company have to measure their human rights impacts and take concrete steps to improve them. The Dutch government states that if a company does business abroad, they are expected to behave responsibly, and take account of the impact of their activities on planet and people.

Oiconomy Pricing is a tool that enables companies on aligning to the various conducts of responsible business by measuring sustainability throughout the supply-chain. Oiconomy Pricing identifies and assesses adverse impacts, provides a platform for mitigation of these impacts, and can monitor a companies’ improvements.

Read more on Responsible Business conduct:

- Government of the Netherlands: Responsible business conduct

- UN Guiding Principles on Business and Human rights (UNGPs)

- OECD Guidelines, including due diligence guidance

- ILO Labour Standards

[/collapse]

B. Working with the tool

[collapse title=”1. What product or service should I select?”]

Any product or service can be assessed using Oiconomy pricing, no matter the company location, industry or size.

Oiconomy Pricing requires the involvement of the main suppliers. Selecting products or services with good supplier relations will make supplier participation easier.

[/collapse]

[collapse title=”2. What product unit should I select?”]

To start the Oiconomy Assessment the organisation needs to select a product and the corresponding unit of that product. It is advised to select a product with a relatively simple supply chain and to consider the willingness of suppliers to contribute to the system.The best product unit (per peace or weight) is usually the one that you already use in your financial bookkeeping, or is the unit that is sold to the consumer.

Example:

To assess coffee the product unit could be 1000 kg, 1kg of coffee or a cup of coffee (14 gram coffee beans). The choice depends on what is easiest for the company.

[/collapse]

[collapse title=”3. How to make the material inventory list?”]

One of the first steps in making the Oiconomy Pricing Assessment is to create a material inventory list of all purchased material and services in relation to the product. This will aid in the selection of suppliers that need to participate in the Oiconomy Pricing Assessment. The list needs to be based on financial bookkeeping and state the costs of purchased product or service to create your final output product. This concerns purchased materials and services only and does not include own personnel costs or operating costs of e.g. machines.

This list needs to include all types of materials purchased for the product such as: packaging materials, components of the product and water.

Example Inventory List: A bar of chocolate from Company A

Total purchased costs/services per bar of chocolate € 1

- Chocolate bar itself (€ 0,76)

- Packaging (€ 0,07)

- Laboratory tests (€ 0,03)

- Transport (€ 0,02)

[/collapse]

[collapse title=”4. Which suppliers need to participate?”]

One product often consists out of resources and parts that come from many different suppliers. Not all of those suppliers need to participate in the Oiconomy Pricing Assessment. In order to find out what suppliers need to participate the 80% rule is applied. The end-producer needs to make a material inventory of all purchased materials and services related to the product (see previous FAQ question). This list needs to be sorted from highest purchased value to lowest.

The largest materials and services that represent 80% of the purchased value need to be included into the assessment. The supply-chain of these products needs to be traced to the origin of the supply-chain, which is the sourcing of the raw materials (mining) or the agricultural stage. The suppliers involved in the identified supply-chains need to apply Oiconomy Pricing to calculate their hidden costs.

An exception to the 80% purchased value rule are high-impact materials. Presence of these high impact materials (either directly purchased or present in the purchased materials) means that the suppliers providing those materials also need to be included directly into the assessment. A list of high-impact materials can be found in the Oiconomy Assessment tool.

Example:

-

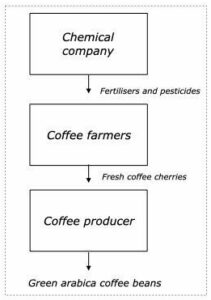

Simple example Coffee Producer: For 1 kg of coffee 80% of the purchased value of coffee is from buying the coffee beans (Figure 3). This means that only the supply-chain of coffee beans needs to be included. These coffee beans come from farmers, which is the origin of the supply-chain. Coffee farmers use a chemical fertiliser, which is a high impact material and therefore also needs to be included in the assessment.

Figure 3: Scope of assessment: Coffee

Figure 3: Scope of assessment: Coffee

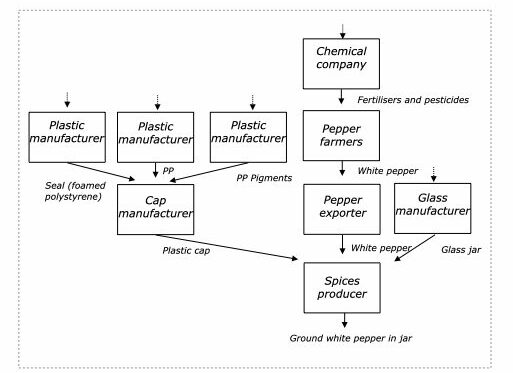

- More complex example Spices Producer: 80% of the purchased value from 1 jar of pepper comes from the pepper, the jar and the cap (Figure 4). The suppliers involved in production of the pepper, the jar and the cap need to be included in the assessment. Pepper farmers, located in the pepper supply-chain also use chemical fertilisers. As this is a high-impact materials – the supplier of fertilisers needs to be included in the assessment, but does not need to be traced back more.

Figure 4: Scope of assessment: Pepper

Figure 4: Scope of assessment: Pepper

[/collapse]

[collapse title=”5. How do I involve my suppliers?”]

Experience has shown us that best way to involve suppliers with Oiconomy Pricing is by leveraging existing supplier relationships, and by explaining how Oiconomy Pricing is a method to jointly work on long-term sustainable supplier relationships. The UU-team can help in reaching out to suppliers.

[/collapse]

[collapse title=”6. How do I work with suppliers that cannot independently execute the Assessment?”]

We realise that not every supplier in the supply-chain is able to complete the Oiconomy Assessment tool, as there may not be capacity.

Oiconomy Pricing has defined “Low-developed supplier” (LDS) as a supplier that is not recognised as a registered or legal body and may not have the knowledge, education or development to independently execute the assessment. If you use an LDS as supplier, the organisation itself is shall collect, demonstrate, and verify the requested data, and take care that the suppliers is potentially included in external audits.

[/collapse]

[collapse title=”7. How should I interpret the results?”]

The results from the Oiconomy Pricing assessment will reveal hidden cost along the supply chain.

The results will:

- Identify all relevant sustainability impacts that happen along the supply-chain

- Express the costs necessary to mitigate all sustainability impacts and have a fully sustainable product

The results do not:

- Indicate which sustainability impacts take priority over other impacts. This means that sustainability impacts that are more expensive to prevent are not more important than the ones that costs less to prevent. We believe that sustainability aspects are interconnected and require a holistic approach to be solved properly.

- Express how much damage your product is causing to planet and people. We express the results in cost to prevent any negative impact and do not measure the damage of your product. We believe this is a more practical and actionable approach, as it makes the data aggregable, comparable, understandable, and more executable by companies themselves.

[/collapse]

[collapse title=”8. Do you have any benchmarks?”]

Not yet. We recognise how valuable it would be to be able to compare your results to similar products. As more cases are gathered, this will be possible in the future.

Partners are invited to contribute to the system to build benchmarks.

[/collapse]

[/collapsibles]