Scientific Justification

Oiconomy Pricing favors full transparency and follows the open science principle. Our methodological principles, calculation rules and data sources are visible for all. Our tool is ready for use, almost inclusive. But it can always be improved. We invite scholars to critically review our approach and possibly suggest refinements. A special invitation stands for anyone that can add to the repository of possible prevention, or mitigation or abatement solutions and their costs per unit of prevented negative impact.

[collapsibles]

[collapse title=”General methodological approach”]

The Oiconomy system consists of:

- The Oiconomy Standard (O.S.), describing the system, included sustainability aspects, assessment criteria and measurement requirements. The O.S. contains the compliance criteria for certification purposes and guidance to the system.

- The Oiconomy Foundation Database (O.F. Database), containing all background data and assumptions.

- The Oiconomy Pricing Tool (O.P.T.), a questionnaire, which, completed by the practitioners, leads to the ESCU scores for the assessed product.

Oiconomy methodology

All aspects, including all industry-relevant SDG’s, are divided in 10 categories, together comprehensively comprising all PPP sustainability aspects.

All ESCU scores are the product of a quantitative factor and a price factor.

The O.S. and the tool guides the practitioner through all aspects, requiring to determine their foreground quantitative aspect and challenges the practitioner to also determine their foreground mitigation price factor and expected mitigation percentage.

Mitigation data need to be based on demonstrable investment proposals or cost calculations.

For both the quantitative and price factors, the system provides background data, which are automatically allocated when foreground data are lacking.

Background quantitative data are obtained from a wide range of globally available databases and available research. The goal of the Oiconomy system is to gradually improve the background data from anonymized results from the system itself.

Background data are determined by means of the following 5-step procedure, derived from the EcoCost methodology https://www.ecocostsvalue.com/:

- Definition of the impact category or subcategory considered, together with the characterization factor, the indicator characterizing the relative weight within the category.

For aspects without items with different impact weights, only an indicator is required. - Determination of the specific standard or target to be achieved.

- Assessment of available effective international standards and conventions.

- Without an effective international standard or no-effect level, 80% reduction of the issue (relative to 1998) or, if concrete measurement of that reduction level is not feasible, at the average level of the 20% best performers (usually countries).

- Where no such concrete target can be defined, the cost distance to perfect governance on the aspect.

The above described target concerns the global level. For each individual actor, the target is usually the local level.

- Listing of major available preventative measures.

- Determination of the costs and net effects of available preventative measures and sorting the list by the costs per one unit of the characterization factor, with the lowest on top.

- Assessment of which preventative measures are required to globally reach the target. The last and most expensive preventative measure to be employed shows the marginal preventative costs. ESCU’s for issues with location dependent impact, the highest costs of major preventative measures, multiplied with a reducing impact dependent multiplication factor is allocated.

References:

Croes, P. R. and Vermeulen, W. J. V. (2015) ‘Life Cycle Assessment by Transfer of Preventative Costs in the Supply Chain of Products. A first draft of the Oiconomy system’, J. Cleaner Prod., 102, pp. 178–187.

[/collapse]

[collapse title=”1. Pollution & Climate”]

General

- Although the climate aspect is usually considered separately and often even presented as the only sustainability issue to be addressed, in the O.S., the global warming potential is considered as only one aspect in the category of pollution.

- Polluting emissions to air, soil or water bodies may occur in four separately covered stages: 1: From organizations’ operations, 2: As industrial waste; 3: As result of the use of the product and 4: At end-of life disposal.

- The aspect of Pollution is divided in 5 subcategories: Types A,B,C,D and E.

- Type A: “Emission of bulk gasses”, causing issues like climate change, acidification, eutrophication, human health issues by fine dust.

- Type B:Hard to measure agricultural emissions.

- Type C:Quantitatively measurable chemical emissions.

- Type D: Thermal Pollution, limited to organizations in power production.

- Type E:Incident caused emissions.

This LCA-aberrant subcategorization was developed to enable foreground assessment of preventative costs for all causes of pollution.

All data for polluting emissions are obtained from the EcoCost/Value system. Justification for the data can be found in https://www.ecocostsvalue.com/. ESCU’s for pollution are equal to EcoCosts.

Impact category and characterization factor

EcoCosts represent the marginal preventative costs for the impact as characterized by a leading indicator. Every midpoint (or subcategory) is characterized by one leading indicator. For this leading indicator, the same 5 step procedure is followed as described above. The EcoCosts for all other emissions within the subcategory are determined by the product of the EcoCosts for the leading indicator and the impact based characterization factor of the concerned chemical. As an example, the EcoCost of emission of methane are calculated as about 30 times the EcoCosts of CO2. In practice, preventative costs of CH4 emissions may be different, because very different preventative measures are required. This is one of the reasons that the O.S. challenges the practitioner to determine the product specific (foreground) preventative measures and -costs for impact mitigation.

Data usources: EcoCosts are available for emissions of individual chemicals, but also for a large range of materials in the Idemat-database. If no quantitative data are available or if even the supplier or country is unknown, the O.P.T. uses data from the Idemat database. The practitioner loses the possibility to correct for double counting preventative costs for pollution and depletion (see O.S. 12.2.13 and O.P.T.-sheet Def-Instr. – I 10).

Targets: The targets are set by either conventions or by European or American standardization authorities.

[/collapse]

[collapse title=”Subcategory 1a: Type A Pollution”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1b: Bulk Gasses”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1c: Electricity”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1d: Fuels (Industrially used)”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1e: Employee Commuting”]

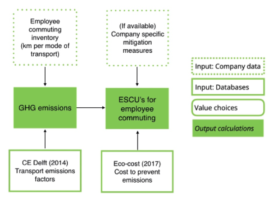

Description

This sub-category measures emissions resulting from the transport of employees between work and their homes. This includes transport from hired labour, temporary employees and permanent employees. Employee commuting represents a major hotspot of greenhouse gas (GHG) emissions worldwide, and accounts for half of all mobility related GHG emissions in the Netherlands (PBL, 2021). Employee commuting is part of scope 3 of the GHG protocol, the global standard for measuring the greenhouse gasses (Greenhouse gas protocol, 2022). From 2023 on, companies in the Netherlands with over 100 employees will have to start tracking how their employees commute to work (Klimaatakkoord, 2019).

Impact category and target

The impact category is the increase in global mean temperature as a result of harmful emissions by employee commuting. The target is the distance to zero emissions resulting from employee transport.

Methodology

Oiconomy pricing measures the ESCU’s of employee travel by calculating the GHG emissions that result from employee transport. The GHG are then transferred into prevention costs, representing the costs necessary to prevent any GHG emissions from employee commuting. There are two main ways of calculating the hidden costs: company-specific data is available or company-specific data not available.

If company-specific data is available on employee commuting, then the hidden costs will be calculated as depicted in Figure X. The company needs to make an inventory of all employee travel related to the product. The employee commuting inventory will be transferred into GHG emissions using emissions factors of vehicles from CE Delft (2014). If company-specific mitigation costs are available, then that will represent the hidden costs to mitigate the GHG emissions. Alternatively, Eco-cost (2017) can be used to transfer the GHG emissions into preventative costs.

When company-specific data are not available the ESCU’s will be calculated by using databases only (Figure X). The calculations start with finding the most likely amount of labour hours per product under review by using the WIOD SEA database. Using Eurostat data, it is then assumed that the employee commutes an average of 37 km by car. This results in an employee commuting inventory that can be calculated into GHG emissions using the transport emissions factors from CE Delft (2014). These GHG emissions are then transferred into hidden cost using Eco-cost (2017).

Figure 1e-a Calculation of employee commuting – company specific data available

Figure 1e-b Calculation of employee commuting – company specific data unavailable

Data sources for performance data

Company-specific data:

- Type of vehicle used per employee

- The type of fuel used in the vehicle

- The amount of km commuted by employees in year X

- Turnover of organization in year X

- Sales price of unit of product

- Turnover of product in year X

Data from databases:

- Labour intensity per unit of product (if company-specific data is unavailable).

The labour intensity of a product can be found through using input output databases such as the WIOD-SEA database. The WIOD-SEA (2016) database lists the labour share for the sector/country combination (which is indicated by “LAB/VA)”. If the country is not listed, the country with closest Human Development Index (HDI) to the potential countries can be taken.

- Emission factors for transport per vehicle.

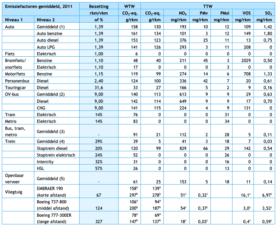

The emission factors per type of vehicle are taken from CE Delft (2014) (Table X). This database gives an overview of the emissions factors of transport in 2011.

- Average commute distance to work (if company-specific data is unavailable.

Using Eurostat (2021) data, an average travel distance to work is total 37 km per day was found.

{kind=link}

Table 1e-a Emissions factors per vehicle type and fuel (Dutch). Source: CE Delft (2014), p.14

Data sources for prevention costs

Company-specific costs:

Companies can present their own costs for specific mitigation measures. Possible mitigation measures are: organizing working from home infrastructure, collective transport or sustainable commuting incentives.

- Cost mitigation measure

- % mitigation as a result of the measure

Costs from databases:

- The Eco-cost database is used to transfer emissions into prevention costs, if company specific mitigation measures are not available. The Eco-cost database is based on marginal prevention costs, meaning that the maximum costs of a list of selected measures to sufficiently tackle a sustainability issue (Eco-cost, 2017). Table X lists the marginal prevention costs and preventative measure per impact category, that is the foundation for calculating prevention costs resulting from emissions from transport.

Table 1e-b Eco-cost model of emissions (Adapted from Eco cost value, n.d.)

| Category | Eco-cost |

Marginal Preventative measure |

Midpoint table |

| eco-costs of global warming | 0.116 €/kg CO2 equivalent |

Sustainable electricity generation by windmills at the North-sea. |

Potential 100 years, IPCC 2013, including climate-carbon feedbacks (EF version) |

| eco-costs of acidification | 8.75 euro / kg SO2 equivalent (= 6.68 euro / mol H+ eq) | Ultra-Low Sulphur Diesel Production in the EU of 10 ppm | EF table (including EU country factors) |

| eco-costs of eutrophication | 4.70 euro / kg PO4 equivalent (= 14.40 euro / kg P eq) | Ultra-Low Sulphur Diesel Production in the EU of 10 ppm | EF table (including EU country factors) |

| Photochemical oxidant formation (‘summer smog’) | 5.35 Euro/ kg NOx equivalent (NMVOS equivalent) = 9.08 euro/kg C2H4 eq) |

2001 – stringent’ emission classification for cars |

LOTOS-EUROS model |

| eco-costs of fine dust | 35.0 €/kg fine dust PM2.5 equivalent | Data for fine dust filters of cars | UNEP/CETAC plus EF table |

| eco-costs of ecotoxicity | 340.0 €/kg Cu equivalent | water treatment costs of smaller industrial systems | UseTox 2 (recommended plus interim), freshwater ecotoxicity (EF version) |

| eco-costs of human toxicity cancer | 3754 €/kg Benzo(a)pyrene equivalent | Spending 80.000 euro per DALY (Disability Adjusted Life Years) as medical costs | UseTox 2 (recommended plus interim), cancer (EF version) |

| eco-costs of human toxicity non-cancer | 25500 €/kg Mercury. equivalent | Spending 80.000 euro per DALY (Disability Adjusted Life Years) as medical costs | UseTox 2 (recommended plus interim), non-cancer (EF version) |

| Ozone layer depletion | 120 € / kg CFC-12 |

The price of refrigerant HFO-1234yf in cooling systems |

The midpoint table for ozone layer depletion: ILCD 2011 Midpoint+ |

Value choices and limitations

- Using emissions factors for vehicles from CE Delft (2014) poses several limitations

- The emissions factor may not be representative for other countries than the Netherlands because of several reasons

- The impact from electricity consumption is based on the electricity mix of the Netherlands.

- Dutch cars are newer than the EU-average, lowering the emission factors.

- Road conditions influence the emissions factor, favourable road conditions in the Netherlands might make the emissions higher elsewhere.

- The development and maintenance of infrastructure for transport are not included.

- The emissions factor may not be representative for other countries than the Netherlands because of several reasons

- Eco-cost (2017) is used to monetize emissions resulting from transport. The costs are derived from the cost of best available technologies that prevent negative impact. These best available technologies can be assumed to be representative for Europe, but are less representative for the rest of the world. Outside of Europe, the most expensive mitigation measure might be more or less costly.

Formulas

ESCU’s = SUM{ mode of transport * km yearly commuting per year for product line} * revenue correction) * (Emission factor per vehicle per km * prevention costs)

References

CE Delft (2014). STEAM personenvoervoer 2014. Studie naar Transport emissies van alle modaliteiten emissiekentallen 2011. Accesible at https://ce.nl/wp-content/uploads/2021/03/CE_Delft_4787_STREAM_personenvervoer_2014_1.1_DEF.pdf

Eco-cost (2017). Ecocosts2017_V1-8_midpoint-tables.xlsx,Delft University. Accessible at https://www.ecocostsvalue.com/EVR/img/Ecocosts2017_V1-8_midpoint-tables.xls

Eco cost value (n.d.). The way eco-costs of emissions are determined https://www.ecocostsvalue.com/eco-costs/eco-costs-emissions/

Eurostat (2021). Distribution of distance travelled per person per day by travel purpose for urban mobility on all days. Accessible at https://ec.europa.eu/eurostat/statistics-explained/index.php?title=File:Distribution_of_distance_travelled_per_person_per_day_by_travel_purpose_for_urban_mobility_on_all_days_Table_3_Feb_2021.png

Greenhouse Gas (GHG) Protocol. (2015). A Corporate Accounting and Reporting Standard. Accessible at https://ghgprotocol.org/sites/default/files/standards/ghg-protocol-revised.pdf

Klimaatakkoord (2019). Den Haag 28 juni 2019. Accessible at https://open.overheid.nl/repository/ronl-7f383713-bf88-451d-a652-fbd0b1254c06/1/pdf/klimaatakkoord.pdf

PBL Plan Bureau voor de Leefomgeving (2021). Thuiswerken en de gevolgen voor wonen, werken en mobiliteit: Op zoek naar trends, trendbreuken en kansen als gevolg van corona. Accessible at https://www.pbl.nl/sites/default/files/downloads/pbl-2021-thuiswerken-en-de-gevolgen-voor-wonen-werken-en-mobiliteit.pdf

WIOD-SEA database. (2016). Accessible at https://www.rug.nl/ggdc/valuechain/wiod/wiod-2016-release

Include: Scientific & societal justification

will be shown soon

[/collapse]

[collapse title=”Subcategory 1f: Business trips”]

Description

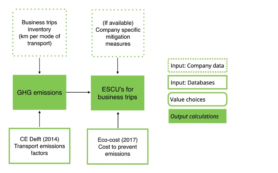

This sub-category measures emissions resulting from business trips. This includes emissions from transportation of employees engaged in business related activities, traveling by aircrafts, train, buses and passenger cars. It is estimated that pre-pandemic business travel constituted of upto 20% of global travel (Borko et al. 2020). Business travel is part of scope 3 emissions ofe the GHG (Greenhouse gas protocol, 2022).

Impact category and target

The impact category is the increase in global mean temperature as a result of harmful emissions by employee commuting. The target is the distance to zero emissions resulting from business travel.

Methodology

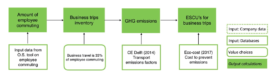

Oiconomy pricing measures the cost of business travel by calculating the GHG emissions that results from business travel. The GHG emissions are then transferred into prevention costs, presenting the cost necessary to prevent any GHG emissions from business trips. There are two main ways to calculate hidden cost for business trips: company-specific data is available or company-specific data is not available.

If company-specific data on business trips is available, then the hidden costs will be calculated as depicted in Figure X. The company needs to make an inventory of all the business trips made in a specific year. The business trips inventory will be transferred in to GHG emissions using the emissions factors of vehicles from CE Delft (2014). If company-specific mitigation costs are available, then that will represent the hidden cost to mitigate the GHG emissions. Alternatively, Eco-cost (2017) can be used to transfer the GHG emissions into preventative costs.

When company-specific data are not available, the hidden costs will be calculated by using databases only (Figure X). The employee commuting inventory (aspect X) is taken as the base for calculation for business trips. The assumption was made that business trips make up a maximum of 33% of the amount of employee commuting from home to work. Based on this assumption the GHG emissions for business trips can be calculated using CE Delft (2013) emissions factors. The GHG are then transferred into hidden cost using Eco-cost (2017).

Figure 1f-a Calculation of business trips – company specific data available

Figure 1fb Calculation of business trips – company specific data unavailable

Data sources performance data

Company-specific data:

- Means of travel for business trips (plane, buses, metro, tram, motorbike passenger cars)

- The type of fuel used in the vehicle

- The amount of km commuted of the business trip

- Turnover of organization in year X

- Sales price of unit of product

- Turnover of product in year X

Data from databases:

- Emission factors for transport per vehicle.

The emission factors per type of vehicle are taken from CE Delft (2014) (Table X). This database provides an overview of the emissions factors of transport in 2011.

Table 1f-a Emissions factors per vehicle type and fuel (Dutch). Source: CE Delft (2014), p.14

Data sources prevention costs

Company-specific costs

Companies can present their own costs for specific mitigation measures. Possible mitigation measures are: organizing working from home infrastructure, or sustainable travel options.

- Cost mitigation measure

- % mitigation as a result of the measure

Costs from databases

- The Eco-cost database is used to transfer emissions into prevention costs, if company specific mitigation measures are not available. The Eco-cost database is based on marginal prevention costs, meaning that the maximum costs of a list of selected measures to sufficiently tackle a sustainability issue (Eco-cost, 2017). Table X lists the marginal prevention costs and preventative measure per impact category, that is the foundation for calculating prevention costs resulting from emissions from transport.

Table 1f-b Eco-cost model of emissions (Adapted from Eco cost value, n.d.)

| Category | Eco-cost |

Marginal Preventative measure |

Midpoint table |

| eco-costs of global warming | 0.116 €/kg CO2 equivalent |

Sustainable electricity generation by windmills at the North-sea. |

Potential 100 years, IPCC 2013, including climate-carbon feedbacks (EF version) |

| eco-costs of acidification | 8.75 euro / kg SO2 equivalent (= 6.68 euro / mol H+ eq) | Ultra-Low Sulphur Diesel Production in the EU of 10 ppm | EF table (including EU country factors) |

| eco-costs of eutrophication | 4.70 euro / kg PO4 equivalent (= 14.40 euro / kg P eq) | Ultra-Low Sulphur Diesel Production in the EU of 10 ppm | EF table (including EU country factors) |

| Photochemical oxidant formation (‘summer smog’) | 5.35 Euro/ kg NOx equivalent (NMVOS equivalent) = 9.08 euro/kg C2H4 eq) |

2001 – stringent’ emission classification for cars |

LOTOS-EUROS model |

| eco-costs of fine dust | 35.0 €/kg fine dust PM2.5 equivalent | Data for fine dust filters of cars | UNEP/CETAC plus EF table |

| eco-costs of ecotoxicity | 340.0 €/kg Cu equivalent | water treatment costs of smaller industrial systems | UseTox 2 (recommended plus interim), freshwater ecotoxicity (EF version) |

| eco-costs of human toxicity cancer | 3754 €/kg Benzo(a)pyrene equivalent | Spending 80.000 euro per DALY (Disability Adjusted Life Years) as medical costs | UseTox 2 (recommended plus interim), cancer (EF version) |

| eco-costs of human toxicity non-cancer | 25500 €/kg Mercury. equivalent | Spending 80.000 euro per DALY (Disability Adjusted Life Years) as medical costs | UseTox 2 (recommended plus interim), non-cancer (EF version) |

| Ozone layer depletion | 120 € / kg CFC-12 |

The price of refrigerant HFO-1234yf in cooling systems |

The midpoint table for ozone layer depletion: ILCD 2011 Midpoint+ |

Value choices and limitations

- To calculate the quantity of business trips without company-specific data a choice was made to take 33% of the employee commuting from work to home. This means that the assumption is made that business trips are 1/3 of total employee commuting from work to home. This is based on

- Using emissions factors for vehicles from CE Delft (2014) poses several limitations

- The emissions factor may not be representative for other countries than the Netherlands because of several reasons

- The impact from electricity consumption is based on the electricity mix of the Netherlands.

- Dutch cars are newer than the EU-average, lowering the emission factors.

- Road conditions influence the emissions factor, favourable road conditions in the Netherlands might make the emissions higher elsewhere.

- The development and maintenance of infrastructure for transport are not included

- The emissions factor may not be representative for other countries than the Netherlands because of several reasons

- Eco-cost (2017) is used to monetize emissions resulting from transport. The costs are derived from the cost of best available technologies that prevent negative impact. These best available technologies can be assumed to be representative for Europe, but are less representative for the rest of the world. Outside of Europe, the most expensive mitigation measure might be more or less costly.

Formulas

ESCU’s = ( SUM{mode of transport * km yearly business trips per year for product line} * revenue correction) * (Emission factor per vehicle per km * prevention costs)

References

Borko, S., Geerts, W., & Wang, H. (2020). The travel industry turned upside down: Insights, analysis and actions for travel executives. Skift Research.

CE Delft (2014). STEAM personenvoervoer 2014. Studie naar Transport emissies van alle modaliteiten emissiekentallen 2011. Accesible at https://ce.nl/wp-content/uploads/2021/03/CE_Delft_4787_STREAM_personenvervoer_2014_1.1_DEF.pdf

Eco-cost (2017). Ecocosts2017_V1-8_midpoint-tables.xlsx,Delft University. Accessible at https://www.ecocostsvalue.com/EVR/img/Ecocosts2017_V1-8_midpoint-tables.xlsx

Eco cost value (n.d.). The way eco-costs of emissions are determined https://www.ecocostsvalue.com/eco-costs/eco-costs-emissions/

Greenhouse Gas (GHG) Protocol. (2015). A Corporate Accounting and Reporting Standard. Accessible at https://ghgprotocol.org/sites/default/files/standards/ghg-protocol-revised.pdf

[/collapse]

[collapse title=”Subcategory 1g: Transport of goods”]

Description

This sub-category measures emissions from the transport of goods. Transport of freight causes 7% of the global carbon emissions and represents 5% of the global GDP (OECSD & ITF, 2015). Transport of the product is part of the Greenhouse gas protocol (Greenhouse gas protocol, 2022).

Impact category and target

The impact category is the increase in global mean temperature as a result of harmful emissions by transport of goods. The target is the distance to zero emissions resulting from transport of goods.

Methodology

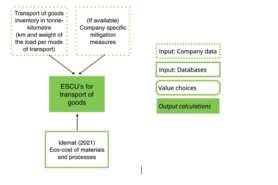

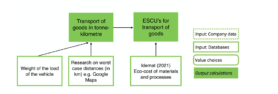

Oiconomy Pricing measures the costs of transport of goods by making an inventory of the amount of km’s the goods travelled and the amount of weight that was transported. This inventory is then transferred into hidden costs. There are two ways of calculating transport of goods: company-specific data is available or company-specific data is unavailable.

If company-specific data are available on transport of goods, then the hidden cost will be calculated as depicted in Figure X. The company needs to make an inventory of the amount of km the goods travelled, the means of transport and the weight of the load. This is expressed in tonne-kilometres (tkm’s). Tonne’s kilometres express 1 tonne being transported for 1 kilometre. In the case of 1kg (0,001 tonne) being transported for 10 km then the equation is 0,001 *10 = 0,01 tm. These tkm’s are then calculated into costs using the Idemat 2021 database (Eco value cost, 2021). In the case that company-specific mitigation costs were calculated, these can be entered into the system directly.

When company-specific data are not available the hidden costs will be calculated by using databases only (Figure X). Through the use of various sources the travel distance of various means of travel can be estimated. The amount of transport in tkm’s per means of travel is then transferred into eco-cost using the Idemat 2021 database (Eco cost value, 2021).

Figure 1g-a Calculation of transport of goods– company specific data available

Figure 1g-b Calculation of transport of goods– company specific data unavailable

Data sources performance data

Data sources performance data

Company-specific data:

- Means of travel (plane, truck, van, tractor, ship)

- The type of plane, truck, van, tractor or ship

- The amount of km commuted (return trip)

- The amount of load per means of travel per trip

- The weight of the product being transported

Data from databases:

- Worst-case travel distance of product

The most probably worst-case distances shall be selected and derived from external data such as google Maps. Sea distances can be calculated using shiptraffic.net. A full load is assumed for the outward journey and a 60% of load is assumed for the inward journey.

Data sources prevention costs

Company-specific costs

The organization can demonstrate the costs (and plan) for the mitigation of emissions by transport of goods (e.g. lower weight, better logistics, more sustainable transport, better logistics).

- Cost mitigation measure

- Exacted mitigation percentage

Costs from databases

- Idemat 2021 data from Eco cost value (2021) is used to calculate the hidden costs resulting from transport of goods. The Idemat dataset contains hidden costs of over a thousand materials and processes. These materials and processes were derived from life cycle inventories from peer reviewed literature, scientific databases and own calculations (Eco cost value, 2021). At the base of these calculation is the eco-cost database (Eco-cost value, 2017). The eco-cost database is used to transfer emissions into prevention costs. The Eco-cost database is based on marginal prevention costs, meaning that the maximum costs of a list of selected measures to sufficiently tackle a sustainability issue (Eco-cost, 2017). Table X lists the marginal prevention costs and preventative measure per impact category, this is the foundation for calculating prevention costs resulting from emissions from transport.

Table 1g-a Eco-cost model of emissions (Adapted from Eco cost value, n.d.)

| Category | Eco-cost |

Marginal Preventative measure |

Midpoint table |

| eco-costs of global warming | 0.116 €/kg CO2 equivalent |

Sustainable electricity generation by windmills at the North-sea. |

Potential 100 years, IPCC 2013, including climate-carbon feedbacks (EF version) |

| eco-costs of acidification | 8.75 euro / kg SO2 equivalent (= 6.68 euro / mol H+ eq) | Ultra-Low Sulphur Diesel Production in the EU of 10 ppm | EF table (including EU country factors) |

| eco-costs of eutrophication | 4.70 euro / kg PO4 equivalent (= 14.40 euro / kg P eq) | Ultra-Low Sulphur Diesel Production in the EU of 10 ppm | EF table (including EU country factors) |

| Photochemical oxidant formation (‘summer smog’) | 5.35 Euro/ kg NOx equivalent (NMVOS equivalent) = 9.08 euro/kg C2H4 eq) |

2001 – stringent’ emission classification for cars |

LOTOS-EUROS model |

| eco-costs of fine dust | 35.0 €/kg fine dust PM2.5 equivalent | Data for fine dust filters of cars | UNEP/CETAC plus EF table |

| eco-costs of ecotoxicity | 340.0 €/kg Cu equivalent | water treatment costs of smaller industrial systems | UseTox 2 (recommended plus interim), freshwater ecotoxicity (EF version) |

| eco-costs of human toxicity cancer | 3754 €/kg Benzo(a)pyrene equivalent | Spending 80.000 euro per DALY (Disability Adjusted Life Years) as medical costs | UseTox 2 (recommended plus interim), cancer (EF version) |

| eco-costs of human toxicity non-cancer | 25500 €/kg Mercury. equivalent | Spending 80.000 euro per DALY (Disability Adjusted Life Years) as medical costs | UseTox 2 (recommended plus interim), non-cancer (EF version) |

| Ozone layer depletion | 120 € / kg CFC-12 |

The price of refrigerant HFO-1234yf in cooling systems |

The midpoint table for ozone layer depletion: ILCD 2011 Midpoint+ |

Value choices and limitations

- The Idemat 2021 database (Eco cost value, 2021) is used to monetize emissions resulting from transport of goods. The costs are derived from the cost of best available technologies that prevent negative impact. These best available technologies can be assumed to be representative for Europe but are less representative for the rest of the world. Outside of Europe, the most expensive mitigation measure might be more or less costly.

Formulas

ESCU’s = tkm *transport means * prevention costs

References

Eco cost value (2021). IdematRevA 2021 database. Accessible at https://www.ecocostsvalue.com/EVR/img/Idemat_2021RevA.xlsx

Eco-cost (2017). Ecocosts2017_V1-8_midpoint-tables.xlsx,Delft University. Accessible at https://www.ecocostsvalue.com/EVR/img/Ecocosts2017_V1-8_midpoint-tables.xlsx

Eco cost value (n.d.). The way eco-costs of emissions are determined https://www.ecocostsvalue.com/eco-costs/eco-costs-emissions/

OECD and ITF (2015) The Carbon Footprint of Global Trade, International Transport Forum: Global dialogue for better transport. Leipzig, Germany; Accessible at https://ec.europa.eu/jrc/en/research-topic/transport-sector-economic-analysis; https://www.returnloads.net/how-to-price-haulage-work/

[/collapse]

[collapse title=”Subcategory 1h: Use pollution”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1i: Type B Pollution (hard to measure agricultural emissions)”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1j: Type C Pollution (measurable chemical emissions)”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1k: Type D Pollution (thermal pollution)”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 1l: Type E Pollution (incident caused pollution)”]

will be shown soon

[/collapse]

[collapse title=”2. Depletion”]

Description

The scarcity of fresh water depends on the location. The marginal preventative measure against depletion of local fresh water is the very expensive seawater desalination with renewable energy and pumped transport to the location. In most cases, cheaper options are available, such as crop choice, planting in pits, evaporation mitigation, soil improvement, local rainwater harvesting, reuse of water, drip technology, desalination of brackish water and long distance transport of available fresh water. The practitioner is challenged to determine his foreground mitigation options, but for the remainder, ESCU’s are allocated based on the marginal measure.`

impact sub-category and indicator: The impact category is depletion of scarce materials and the indicator is the quantity of used fresh water. The characterization factor depends on the local scarcity of water. A BWD (see below) < 0,1 is not considered scarce.

Formula

ESCU’s = Max{(BWD – 0,1) x Q x (WDC + CT),0} , where:

Q = The quantity of lost fresh water as defined above.

EL = The elevation of the location of water use in meters.

DL = The shortest distance to a sea with open connection to an ocean of the location in kilometers.

BWD = The Aqueduct Atlas water scarcity factor (https://www.wri.org/applications/aqueduct/water-risk-atlas).

CT = The costs of transport (pumping) the water from sea to the location with renewable energy, which is calculated, using EL and DL and the data for horizontal and vertical transport in (Zhou & Tol, 2005).

WDC = is the seawater desalination costs with renewable energy: WDC = MIN(D_WNR + DPC x CSP).

D_WNR = the ESCU’s for desalination with not renewable energy of 1 m3 of seawater and can be found in O.F.-07 Scarce Resources.

DPC = the Required Power Consumption for 1 m3 of desalinated water is obtained from http://www.lenntech.nl/kostenberekening-ontziltingsinstallatie.htm (corrected for renewable energy)

CSEP is the country specific ESCU allocation for 1 kwH of power and can be found in O.F.-05 Energy resources.

The country specific WDC in O.F.-07, column Q, is calculated based on the country specific average energy mix; If self-use of renewable energy can be demonstrated, WDC can be calculated with the data in O.F.-07 Scarce Resources.

The formula also shows that If BWD <= than 0,1, the water is not considered scarce and the ESCU’s zero. Literature shows values of both 0,1 and 0,2 for locations without water scarcity.

Water Reuse

One potential mitigation is reuse of the water. Examples: Before-used water can be used for irrigation in agriculture, parks or gardens, toilet flushing, industrial processing, surface cleaning of roads or environmental restoration. If water is reused, the ESCU’s are divided by 2 for both first and next user. Preliminarily, it is assumed that water is not reused more than 1 time.

[/collapse]

[collapse title=”3. Land use”]

Description

Most LCA methodologies consider “land use”, as land degradation, characterized by biodiversity or soil carbon content, following the aim of “land sharing”, combined human activities and nature on the same piece of land. However, literature shows a fierce debate between advocates of “land sparing” and “land sharing”. Land sharing resulting in lower yields increases the risk of new clearing of ecosystems elsewhere. Therefore, the O.S. covers both “land occupation” and “land degradation”. Land occupation is characterized by the yield and land degradation by biodiversity.

Land occupation makes the organization responsible for providing (products, biodiversity, or both).

50% of habitable land is used for agricultural purposes and 37% is forestry, 30% of which is used as production forestry. Only 1% is urban and build-up area. Therefore, considering land use aspects, the O.S. calculations of background ESCU’s is based on agricultural purposes.

The O.S. section on land occupation assesses the distance to an average yield.

Impact category and characterization factor: The impact category is loss of valuable ecosystems by inefficient land use. The characterization factor is the distance to an average crop yield.

Target: The land sparing target is zero cause of further loss of valuable ecosystems or “land degradation neutrality” as set at the RIO conference on sustainable development (United Nations, 2012).

The O.S. seeks a balance between land sparing and land sharing by striving towards sustainable intensive agriculture and allocates ESCU’s for both below-average yields (category land occupation), emission of harmful chemicals (category pollution) and for biodiversity below 80% of locally natural biodiversity (category land degradation/biodiversity). As default value at lacking yield data, 50% of the average yield is assumed (the lowest % mentioned in literature for the relative yield of organic crops).

Indicator: the distance between the yield and the average crop yield in FAOSTAT (www.fao.org/faostat/en/#data/QC). The marginal measure is to compensate the yield shortage by restoration back to the local natural ecosystem and maintenance of the occupied piece of land.

On the aspect of biodiversity, the EcoCost system allocates EcoCosts based on the costs of restauration a piece of land back to the locally natural ecosystem, because this measure prevents loss of biodiversity. The O.S. uses these EcoCosts as background data (see the section on biodiversity). The next section (on land degradation/biodiversity) discusses this method.

In case of a yield gap, extra land is required to compensate for the loss of food. Therefore, extra ESCU’s need to be allocated for restoration of an extra piece of land. Preliminarily, these costs are assumed equal to the costs of restauration of the ecosystem. However, probably, because a continuous flow of considerable amounts of water is required for sustainable arable land, the real costs will even be higher.

The 2018 gross cost of nature and landscape management (excluding purchase of land) for 498956 ha. in the Netherlands was € 1160 million, which is € 2325/ha., including a great variety of landscapes, but excluding water ecosystems. Average European one-off costs on land conversion (excluding purchase of land) were estimated € 1028/ha.y. This makes a total costs of land restoration and maintenance estimated at € 3353/ha.y.

Formula:

ESCU’s =Q x (1-CY/AY) x RC

AY = Average Yield

CY = actual Crop Yield (or product yield)

RC = restoration costs per hectare

Q = quantity of occupied hectares

References

United Nations. (2012). Rio+20 United Nations Conference on Sustainable Development. United Nations, 38164(June), 1–53. https://doi.org/12-38164* (E) 220612

Zhou, Y., & Tol, R. S. J. (2005). Evaluating the costs of desalination and water transport. Water Resour. Res., 41(3), 1–10. https://doi.org/10.1029/2004WR003749

Bodem gebruik in Nederland. (https://opendata.cbs.nl/statline/#/CBS/nl/dataset/70262ned/table?dl=583C6 )

[/collapse]

[collapse title=”Subcategory 3a: Type Land occupation for agricultural or forestry-for -food purposes”]

will soon be shown

[/collapse]

[collapse title=”Subcategory 3b: Land occupation for non-food forestry products”]

will soon be shown

[/collapse]

[collapse title=”Subcategory 3c: Land occupation for non-agricultural products”]

will soon be shown

[/collapse]

[collapse title=”4. Biodiversity”]

Subcategory 4a: Biodiversity Degradation on Land

Information

Many human activities, and especially agriculture go at the expense of biodiversity.

The O.S. challenges the partitioner to determine biodiversity, characterized by the relative count of vascular plants to the locally natural count. Because this count depends on the size of the investigated piece of land, the O.S. requires to sample 10 random chosen pieces of 10 m2 in each hectare of occupied land.

The Ecocost system provides a methodology based on the formula: EcoCosts = X x RC x Q/Q threshold.

RC = the restauration costs per unit of land.

X = the amount of units of land.

Q = the diversity (amount) of vascular plants measured in a unit of land.

Q threshold = the diversity of vascular plants of the locally natural ecosystem.

Because the counted diversity increases with the size of the sampled land, the measurement must be standardized.

References

United Nations. (2012). Rio+20 United Nations Conference on Sustainable Development. United Nations, 38164(June), 1–53. https://doi.org/12-38164* (E) 220612

Zhou, Y., & Tol, R. S. J. (2005). Evaluating the costs of desalination and water transport. Water Resour. Res., 41(3), 1–10. https://doi.org/10.1029/2004WR003749

Impact category and characterization factor:

The impact category is biodiversity and the characterization factor

Subcategory 4b: Biodiversity Degradation in Sea

will be shown soon

[/collapse]

[collapse title=”5. Disposal and Waste”]

will be shown soon

[/collapse]

[collapse title=”6. Human Health”]

will be shown soon

[/collapse]

[collapse title=”7. Labour”]

intro will be shown soon

[/collapse]

[collapse title=”Subcategory 7a: Remuneration”]

Description

This sub-category measures whether the organization provides a fair minimum to their employees and self-employed workers. Article 25.1 of the United Nations Universal Declaration of Human Rights of 1948 states: Everyone has the right to a standard of living adequate for the health and well-being of himself and of his family, including food, clothing, housing, medical care, necessary social services, and the right to security (UN General Assembly 1948). These conventions and statements demonstrate international agreement on the right to a decent minimum wage.The right to a fair remuneration for a worker and his family has been agreed upon in a range of international conventions and translated into national regulations (Anker, 2011).

Many support the concept of the living wage, but it also lack a proper measurement and of a concrete definition as an excuse for not executing their aspirations (Anker 2011, pp. 7,8).

In practice, however, apart from the fact that the minimum wage is widely disrespected and poorly enforced, statutory minimum wages of many countries are below a living wage.

We conclude that conventions and NGOs agree on the need for a minimum wage based but there is a lack of proper measurement and concrete definition (Croes & Vermeulen, 2016a). Croes & Vermeulen (2016ab) came up with a methodology to determine a fair minimum wage (FMW) per country. This methodology is also adopted in Oiconomy Pricing. Croes & Vermeulen (2016ab) set a fair minimum wage based on two points of view: absolute poverty and of relative poverty. The methodology will be described in more detail below.

Impact category and target

The impact category is the increase in income inequality and poverty as a result of wages under the fair minimum. The target is the cost distance to a fair wage.

Methodology

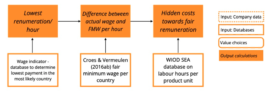

Oiconomy Pricing measures the costs towards fair renumeration for all employees. The difference between the current wage and fair minimum wage are measured, representing the cost necessary to pay everybody a minimum of a fair minimum wage. There are two main ways of calculating the hidden costs: company-specific data is available or company-specific data is not available.

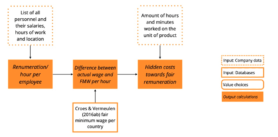

If company-specific data are available, then the hidden cost will be calculated as depicted in Figure X. The company needs to make a list of all personnel containing their salaries, hours of work and location. Using the fair minimum wage determined by Croes & Vermeulen (2016ab), the difference between the actual wage and the fair minimum wage per hour will be calculated. If actual wages are lower than the fair minimum wage then the hidden cost represent the cost-distance to raising all salaries to the fair minimum wage. In the last step the amount of hours and minutes worked on the product need to be provided, so that the extra cost necessary to raise all salaries to the fair minimum wage per product is calculated.

When company-specific data are not available the hidden costs will be calculated by using databases only (Figure X). Using the wage indicator, an organization can determine the most likely lowest payment that is received for production of the product per hour. Using this data, the increase in wage per hour necessary to reach the fair minimum wage can be calculated. In order to calculate the costs to raise salaries to the fair minimum wage per product unit, the number of hours and minutes spend on making one product unit need to be estimated. This can be done using the WIOD Sea database.

Figure 7a-1 Calculation of fair renumeration per product unit– company specific data available

Figure 7a-2 Calculation of fair renumeration– company specific data unavailable

Data sources performance data

Company-specific data:

- List of all personnel and their salaries, hours of work and location.

A list shall be made that lists all workers <20 years old, including manager and self-employed workers that work on the product. The list should specify their gross wage Including (including vacation pay and other bonuses), bonusses, granted shares, including manager and self-employed workers that work on the product and options, contribution to pension.

- All the data should be expressed in payment per hour

- Not included are dividends and differences between realized and granted shares or options from amounts that are already in the possession of the employee.

- For workers paid by piece rate, determine their average wage per hour achievable under healthy conditions and stress levels are long term workhours.

- Number of hours and minutes worked on the product (directly and indirectly).

Calculate the amount of hours and minutes worked on the product per unit of product. If available, this should be equal to a companies; direct and indirect hour used for standard costs allocations.

Data from databases:

- Wage indicator

The lowest payment/hour for the labour in the most likely country can be found at www.wageindicator.org. In the wage indicator the payment/hour are presented as a range and the lowest wage should be selected. If the data cannot be found in wageindiactor.org, alternative databases can be used.

Data sources prevention costs

Costs from databases

- Fair minimum wage based on Croes & Vermeulen (2016ab).

Croes & Vermeulen (2016ab) determined a fair minimum wage per country. This was based on two indicators: absolute poverty and relative poverty. Absolute poverty is when a household income is too low to meet basic needs such as food, shelter, safe drinking water, education and healthcare. For countries experiencing absolute poverty, the fair minimum wage was determined to reflect a minimum amount that provides basic needs. Relative poverty is a situation when the income are so inadequate as they are excluded from having an acceptable standard of living considering the society in which they live (Council of the European Union, 2004). This type of poverty is measured as a proportion of the national income. The justification of the absolute poverty line and the relative poverty line will be discussed below.

- Absolute poverty line

Absolute poverty and the therefrom derived living wage are usually measured by the costs of a basket of basic needs of a person. An abundance of researchers has demonstrated that living wages differ by country, culture, development level, region and even by town, arguing that it is impossible to set one universally applicable and fair global minimum wage. The World Bank solves the price issue by the use of the purchase power parity (PPP) which compares what people in the different locations can buy with their local currency with the value of one US$ in a set reference year.

The Moderate Poverty Line of the World Bank (2016) represents the most universal threshold for setting a fair minimum wage for absolute poverty. The poverty line is based on the cost of essential resources that an average adult consumes in a year. We decided to take the poverty line for lower-middle income countries of $3,20 per day p.p (PPP), as a foundation for the fair minimum wage (Table X). This poverty line however needs to be corrected for the labour contribution ratio and needs to be corrected for the fact that a person is restricted to working in their working years only. The labour contribution ratio represents the income that a household loses by having children, as it is assumed that one of the two adults only earns half, one half of their working years in order to take care of children. In order to correct for this loss of income, the fair minimum wage needs to increase with a factor of 1,25. The LE/WY equation presents the fact that one person only working an average of 46,21 years over an average lifetime of 78,34 years. This means that on average, every person has to gain 1,70 times a living income in their lifetime. Following the equation this means that the fair minimum wage is= 365 * $3,20*1,25*1,70 = $2482 US PPP in 2011. This means that the fair minimum wage of any country needs to be equal to a yearly salary of $2482 in 2011 in the US.

Table 7a-a: Formula to determine Absolute Fair Minimum income (Croes & Vermeulen, 2016b)

| AMWy is: AMWy = (365 * MPL * LCR * (LE/WY)

AMW: Absolute yearly minimum wage MPL: Moderate poverty line LCR: Labour contribution ratio LE: life expectancy WY: working years |

- Relative poverty line

more will be shown soon

References

Anker R (2011) Conditions of work and employment programme estimating a living wage: a methodological review. Int Labour Off 29: 1–126

UN General Assembly (1948) Universal declaration of human rights. United Nations, pp 1–6

Council of the European Union (2004) Joint report by the Commission and the Council on social inclusion, no. 7101/04, Bruxelles

Croes, P. R., & Vermeulen, W. J. (2016a). In search of income reference points for SLCA using a country level sustainability benchmark (part 1): fair inequality. A contribution to the Oiconomy project. The International Journal of Life Cycle Assessment, 21(3), 349-362.

Croes, P. R., & Vermeulen, W. J. (2016b). In search of income reference points for SLCA using a country level sustainability benchmark (part 2): fair minimum wage. A contribution to the Oiconomy project. The International Journal of Life Cycle Assessment, 21(3), 363-377.

[/collapse]

[collapse title=”Subcategory 7b: Inequality”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 7c: Child Labor”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 7d: Overtime”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 7e: Health insurance”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 7f: Personnel Development”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 7g: Employment contract time”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 7h: Various Labor-related aspects”]

will be shown soon

[/collapse]

[collapse title=”8. Social aspects”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 8a: Animal welfare”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 8b: Social aspects User Phase”]

will be shown soon

[/collapse]

[collapse title=”9. Economic fairness”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 9a: Fair Transactions”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 9b: Transparency”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 9c: Fair Tax Contributions”]

will be shown soon

[/collapse]

[collapse title=”Subcategory 9d: Finance related criteria”]

will be shown soon

[/collapse]

[collapse title=”10. Corruption & Conflict”]

will be shown soon

[/collapse]

[collapse title=”Bonus for positive contributions”]

will be shown soon

References

Croes, P. R. and Vermeulen, W. J. V. (2021) ‘The Assessment of Positive Impacts in LCA in general and in Preventative Cost-based LCA in particular . A contribution to the Oiconomy Project’, Int. J. Life Cycle Assess, 2021, 26(1), pp. 143–156

[/collapse]

[/collapsibles]